LMI (Lenders Mortgage Insurance) Explained: What It Costs & How to Avoid It

What Is Lenders Mortgage Insurance (LMI)?

Understanding LMI: Who It Protects and Why

Lenders Mortgage Insurance (LMI) is a one-off insurance premium that protects your lender — not you — in case you default on your home loan and the property sells for less than the outstanding loan balance. Despite the fact that the borrower pays for it, LMI exists solely to protect the bank's financial exposure on higher-risk loans.

If that sounds a bit unfair, you're not alone in thinking so. LMI is one of the most misunderstood costs in the home-buying process, and many first-time buyers in Williams Landing and Point Cook are surprised to learn about it. But understanding how it works — and how to avoid it — can save you tens of thousands of dollars.

When Is LMI Required?

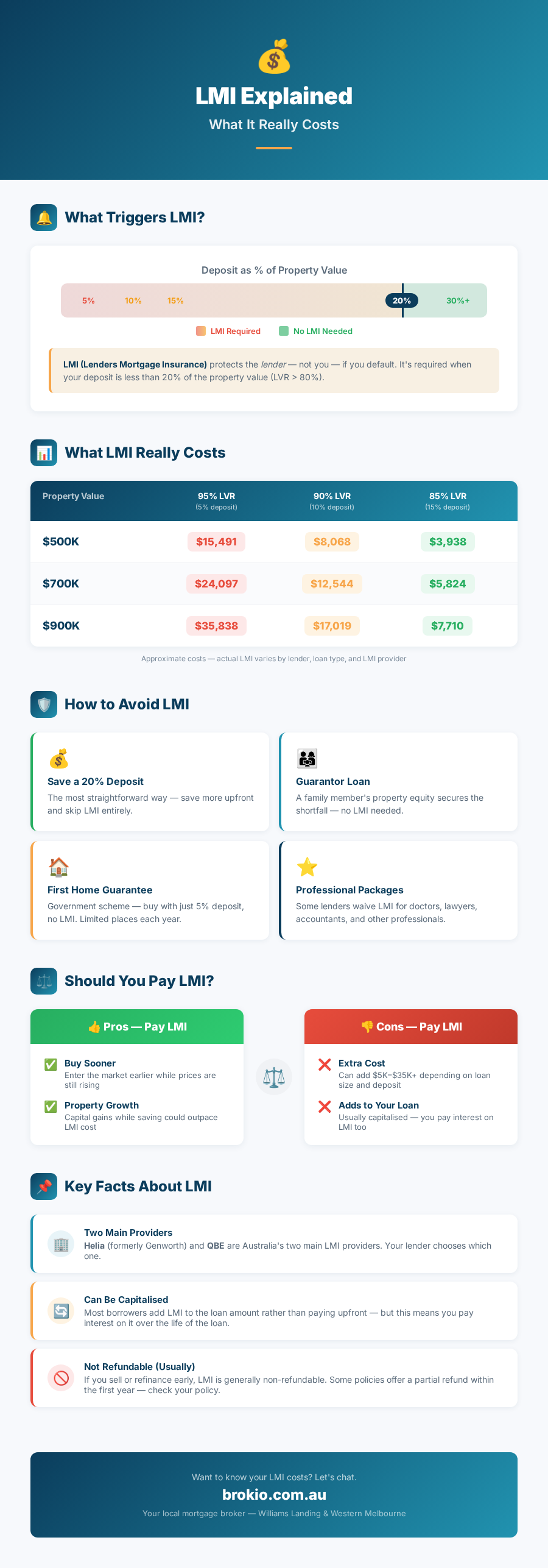

LMI is typically required when your deposit is less than 20% of the property's value. In lending terms, this means your Loan-to-Value Ratio (LVR) exceeds 80%. The higher your LVR, the riskier the loan is considered — and the more LMI costs.

Here's a quick breakdown:

- LVR of 80% or below (20%+ deposit): No LMI required

- LVR of 80.01% to 85% (15–20% deposit): LMI applies — moderate cost

- LVR of 85.01% to 90% (10–15% deposit): LMI applies — higher cost

- LVR of 90.01% to 95% (5–10% deposit): LMI applies — highest cost

- LVR above 95%: Most lenders won't approve the loan at all

Who Provides LMI in Australia?

There are two main LMI providers in Australia:

- Helia (formerly Genworth): Australia's oldest LMI provider, established in 1965. Used by many major lenders including CommBank and Westpac.

- QBE Lenders' Mortgage Insurance: Used by NAB, ANZ, and many non-major lenders.

Some large banks, particularly CommBank, also have their own self-insurance arrangements, which means they underwrite LMI internally rather than going through Helia or QBE. The LMI premium can vary between providers and between lenders, which is one reason why comparing options through a mortgage broker is so valuable.

LMI Is NOT the Same As...

Let's clear up some common confusion:

- LMI ≠ Home and Contents Insurance: Home insurance protects your property and belongings. LMI protects the lender.

- LMI ≠ Landlord Insurance: Landlord insurance covers rental property risks (tenant damage, loss of rent). LMI is unrelated.

- LMI ≠ Income Protection Insurance: Income protection covers you if you can't work due to illness or injury. LMI doesn't help you at all if you lose your job.

- LMI ≠ Mortgage Protection Insurance: Some insurers offer products that cover your loan repayments in specific circumstances. LMI doesn't do this.

The key takeaway: you pay for LMI, but it only benefits the lender. That's exactly why it's worth understanding how to minimise or avoid it entirely.

How LMI Is Calculated: Factors That Determine Your Cost

The LMI Calculation Formula

LMI isn't a simple flat percentage — it's calculated on a tiered scale that takes multiple factors into account. Understanding these factors helps you estimate your costs and identify strategies to reduce them.

Factor 1: Loan-to-Value Ratio (LVR)

This is the single biggest driver of LMI cost. The higher your LVR (i.e., the smaller your deposit), the more you'll pay. LMI premiums increase significantly as LVR moves above 80%, with steep jumps at the 85%, 90%, and 95% marks.

For example, on a $700,000 property:

- 85% LVR (15% deposit of $105,000): LMI ≈ $17,350

- 90% LVR (10% deposit of $70,000): LMI ≈ $26,740

- 95% LVR (5% deposit of $35,000): LMI ≈ $30,797

The jump from 85% to 95% LVR nearly doubles the LMI premium. This is why even a small increase in your deposit can yield significant savings.

Factor 2: Loan Amount

LMI is calculated as a percentage of the loan amount, not the property value. A larger loan means a higher premium. The percentage applied varies based on the LVR tier.

Factor 3: Property Type

The type of property you're buying affects your LMI cost:

- Established houses: Standard LMI rates

- New builds/house and land: Standard rates, sometimes slightly lower

- Apartments and units: May attract higher LMI premiums, especially for smaller units or those in high-density buildings

- Vacant land: Higher LMI rates due to perceived higher risk

- Rural properties: May attract higher premiums or be ineligible for standard LMI

Factor 4: Loan Purpose

Whether you're buying as an owner-occupier or investor affects your LMI:

- Owner-occupier (principal and interest): Standard LMI rates

- Investor loans: Typically 15–30% higher LMI premiums than equivalent owner-occupier loans

- Interest-only loans: May also attract higher premiums

Factor 5: First Home Buyer Status

Some lenders offer LMI discounts for first home buyers, particularly through specific products designed for this market. Additionally, government guarantee schemes (discussed in detail later) can eliminate LMI entirely for eligible first home buyers.

Factor 6: The Lender and LMI Provider

LMI costs vary between lenders because:

- Different lenders use different LMI providers (Helia vs QBE vs self-insured)

- Some lenders negotiate bulk discounts with their LMI provider

- Some lenders add a margin on top of the LMI premium

- Professional packages at some lenders include LMI discounts or waivers for certain occupations

This is a crucial reason to compare options. A mortgage broker can show you the exact LMI cost across multiple lenders — and sometimes the difference is thousands of dollars for the exact same property and deposit.

Real LMI Cost Examples for Williams Landing & Point Cook

What LMI Actually Costs on Local Property Prices

Let's look at realistic LMI costs for properties in the Williams Landing and Point Cook area. These estimates are based on 2026 data from major lender calculators for owner-occupier, principal-and-interest loans on established residential property.

Scenario 1: $600,000 Apartment in Williams Landing

A first home buyer purchasing a two-bedroom apartment with different deposit amounts:

- 20% deposit ($120,000) — 80% LVR: LMI = $0

- 15% deposit ($90,000) — 85% LVR: LMI ≈ $12,850

- 10% deposit ($60,000) — 90% LVR: LMI ≈ $22,835

- 5% deposit ($30,000) — 95% LVR: LMI ≈ $26,305

The difference between a 10% and 20% deposit on this property is nearly $23,000 in LMI alone. That's a powerful incentive to save a larger deposit — or to explore the government guarantee schemes discussed below.

Scenario 2: $700,000 House in Point Cook

A couple buying their first three-bedroom house:

- 20% deposit ($140,000) — 80% LVR: LMI = $0

- 15% deposit ($105,000) — 85% LVR: LMI ≈ $17,350

- 10% deposit ($70,000) — 90% LVR: LMI ≈ $26,740

- 5% deposit ($35,000) — 95% LVR: LMI ≈ $30,797

Scenario 3: $800,000 Family Home in Williams Landing

A family upgrading to a four-bedroom home near Williams Landing train station:

- 20% deposit ($160,000) — 80% LVR: LMI = $0

- 15% deposit ($120,000) — 85% LVR: LMI ≈ $21,850

- 10% deposit ($80,000) — 90% LVR: LMI ≈ $31,900

- 5% deposit ($40,000) — 95% LVR: LMI ≈ $35,554

Scenario 4: $900,000 Property in Point Cook

Buying near the upper end of the local market:

- 20% deposit ($180,000) — 80% LVR: LMI = $0

- 15% deposit ($135,000) — 85% LVR: LMI ≈ $26,350

- 10% deposit ($90,000) — 90% LVR: LMI ≈ $36,060

- 5% deposit ($45,000) — 95% LVR: LMI ≈ $40,080

The Deposit-LMI Trade-Off

Looking at these numbers, a pattern becomes clear: every extra 5% you add to your deposit dramatically reduces LMI costs. For an $800,000 property, increasing your deposit from 10% to 15% saves approximately $10,050 in LMI. Going from 15% to 20% saves you the entire $21,850 because LMI drops to zero.

But here's the counterpoint: saving that extra deposit takes time. If property prices in Williams Landing are growing at 5–10% per year, waiting 12 months to save an additional $40,000 could mean the property you're looking at has increased by $40,000–$80,000. In a rising market, paying LMI and buying sooner can sometimes be the smarter financial decision. This is exactly the kind of analysis a mortgage broker can help you work through.

Paying for LMI: Upfront vs Capitalised Into Your Loan

Option 1: Capitalise LMI Into Your Home Loan

The most common way Australians pay for LMI is by adding it to their home loan balance. This is called capitalising the LMI premium. The lender pays the LMI provider on your behalf and then adds the cost to your total loan amount.

Advantages:

- No upfront out-of-pocket cost — you don't need extra cash at settlement

- Spreads the cost over the life of the loan, making it more manageable

- Allows you to use all your savings for the deposit itself

Disadvantages:

- You pay interest on the LMI amount over the life of the loan

- This significantly increases the total cost — a $25,000 LMI premium capitalised over 30 years at 6% costs approximately $54,000 in total (the premium plus ~$29,000 in interest)

- Your LVR increases slightly because your loan balance is now higher

Option 2: Pay LMI Upfront

You can choose to pay the LMI premium as a lump sum at settlement, separate from your home loan.

Advantages:

- No interest charged on the LMI amount — it's a one-off payment

- Your total loan amount is lower, meaning lower monthly repayments

- You'll pay significantly less over the life of the loan

Disadvantages:

- Requires extra cash at settlement, on top of your deposit, stamp duty, legal fees, and other costs

- Fewer buyers have this much cash available, especially first home buyers

The Real-World Cost Difference

Let's use a worked example for an $800,000 property with a 10% deposit ($80,000), meaning a $720,000 loan with approximately $31,900 in LMI:

If you capitalise the LMI:

- Total loan amount: $751,900 ($720,000 + $31,900)

- Monthly repayments at 6.0% over 30 years: ~$4,507

- Total interest over 30 years: ~$871,620

- Total cost of the loan (principal + interest): ~$1,623,520

If you pay LMI upfront:

- Total loan amount: $720,000

- Monthly repayments at 6.0% over 30 years: ~$4,316

- Total interest over 30 years: ~$833,760

- Total cost of the loan: ~$1,553,760 + $31,900 upfront = ~$1,585,660

Saving by paying upfront: Approximately $37,860 over the life of the loan. That's the interest you'd pay on the capitalised LMI amount.

Which Option Is Right for You?

For most first home buyers in Williams Landing and Point Cook, capitalising LMI is the practical choice — you're already stretching to cover the deposit and stamp duty, and finding an extra $20,000–$35,000 in cash simply isn't feasible. However, if you do have the funds available (perhaps from a gift or inheritance), paying upfront saves you real money.

Alternatively, you can adopt a hybrid strategy: capitalise the LMI now, but make extra repayments early in the loan to pay off the LMI component quickly. By paying an additional $500–$1,000 per month in the first year or two, you can eliminate the LMI balance before significant interest accrues. At Brokio, we help clients model these scenarios so you can see exactly what each option costs and make an informed decision.

6 Ways to Avoid Paying LMI

Strategy 1: Save a 20% Deposit

The most straightforward way to avoid LMI is to save a deposit of 20% or more of the property value. For a $700,000 home in Point Cook, that's $140,000. For an $800,000 home in Williams Landing, it's $160,000. It's a significant sum, and it can take years to save — but it completely eliminates LMI, gives you access to better interest rates, and results in lower monthly repayments.

Tips for saving faster:

- Set up a dedicated high-interest savings account and automate regular transfers

- Take advantage of salary sacrifice into super and then access the First Home Super Saver (FHSS) Scheme to withdraw up to $50,000 in voluntary contributions for your deposit

- Reduce discretionary spending and redirect the savings

- Consider a side income or temporary lifestyle changes to accelerate your savings timeline

Strategy 2: Use the First Home Guarantee (Expanded from October 2025)

This is a game-changer for first home buyers. The Australian Government's First Home Guarantee (formerly the First Home Loan Deposit Scheme) was significantly expanded from 1 October 2025. The key changes mean:

- No income caps: The previous limits of $125,000 (individual) and $200,000 (couple) have been removed

- No cap on places: Previously limited to 35,000 spots per year — now available to all eligible first home buyers

- 5% deposit, no LMI: The government guarantees up to 15% of the property value, allowing you to borrow 95% LVR without paying LMI

- Property price caps apply: In Melbourne, the cap is $800,000 for the First Home Guarantee

For first home buyers in Williams Landing and Point Cook, this scheme is incredibly powerful. You could purchase a $700,000 property with just a $35,000 deposit and pay zero LMI — a saving of approximately $30,000.

Strategy 3: Get a Family Guarantee (Guarantor Loan)

A family guarantee (or guarantor loan) allows a family member — usually a parent — to use the equity in their own property as additional security for your loan. This effectively brings your LVR below 80%, eliminating the need for LMI.

- The guarantor doesn't give you cash — they provide a limited guarantee secured against their property

- Once you've built enough equity (typically when your LVR drops below 80%), the guarantor can be released from the loan

- The guarantee is usually limited to 20% of your property value, minimising risk for the guarantor

Strategy 4: Professional Packages and LMI Waivers

Several lenders offer LMI waivers or significant discounts for borrowers in certain professions. Common eligible professions include:

- Medical professionals (doctors, dentists, veterinarians, pharmacists)

- Legal professionals (solicitors, barristers)

- Accountants (CA or CPA qualified)

- Engineers

- Some IT professionals and senior executives

These waivers can apply for LVRs up to 85% or even 90%, saving you thousands. If you or your partner work in one of these fields, ask your broker about professional packages.

Strategy 5: Negotiate with Your Lender

While LMI rates are largely standardised, there's sometimes room to negotiate — particularly if you're borrowing a large amount or have a strong credit profile. Some lenders may offer risk-based pricing that results in lower LMI for lower-risk borrowers.

Strategy 6: Consider a Different Property Strategy

If you're close to the 20% deposit threshold, consider whether adjusting your property target could eliminate LMI entirely. For example, if you have $130,000 saved and are looking at $700,000 properties (LVR ~81.4% = LMI required), purchasing at $650,000 instead brings your LVR to exactly 80% — and your LMI drops to $0. The $50,000 lower purchase price plus the LMI saving of ~$17,000 means you're $67,000 better off.

LMI FAQs, Refunds & How Brokio Can Help

Can You Get an LMI Refund?

This is one of the most common questions we get at Brokio. The short answer: maybe, but it depends.

If you repay your home loan in full within the first 1 to 2 years (for example, by selling the property or refinancing), you may be entitled to a partial refund of your LMI premium. Here's what you need to know:

- Helia: Depending on your lender's arrangement, a partial refund may be available if the loan is paid out within 2 years of settlement. The refund decreases over time and is typically processed through your lender, not directly.

- QBE: Similar policies apply — partial refunds may be available within the first 2 years, but the specifics depend on the agreement between QBE and your lender.

- Self-insured lenders (e.g., CommBank): Refund policies vary and may differ from the external providers.

- Important: The refund request must typically be made within a specific timeframe after the loan is repaid. Don't assume it will happen automatically — ask your lender or broker to initiate the refund request.

If you're planning to sell or refinance within the first couple of years, make sure you understand the refund terms before settlement. Your Brokio broker can clarify this for you.

Is LMI Tax-Deductible?

If the property is an investment property, the LMI premium is generally tax-deductible — but not as a lump sum in the year you pay it. Instead, it must be spread over the lesser of 5 years or the remaining loan term. For owner-occupied properties, LMI is not tax-deductible. Always consult your accountant for advice specific to your situation.

Does LMI Transfer If You Refinance?

No. LMI is not portable. If you refinance your home loan to a different lender, your existing LMI policy does not transfer. If your LVR at the new lender is still above 80%, you'll need to pay LMI again with the new lender. This is a critical consideration when weighing up refinancing options — the potential interest rate savings need to outweigh the cost of paying LMI a second time.

Is It Worth Paying LMI to Get Into the Market Sooner?

This is the million-dollar question, and the answer depends on your personal circumstances and market conditions. In a rising market — like Melbourne's western suburbs have experienced — buying sooner with LMI can sometimes be financially better than waiting to save a 20% deposit. Here's why:

- If property prices are growing at 5–7% per year, an $800,000 home today could be worth $840,000–$856,000 in 12 months

- The $31,900 LMI cost may be less than the price increase you'd face by waiting

- You start building equity and stop paying rent immediately

However, in a flat or declining market, waiting to save a larger deposit avoids the LMI cost and reduces your risk. This is where professional advice from a broker becomes invaluable.

How Brokio Helps You Navigate LMI

At Brokio, we don't just calculate your LMI — we help you understand whether it makes sense to pay it, avoid it, or minimise it. Here's what we do for our clients in Williams Landing, Point Cook, and Melbourne's western suburbs:

- Compare LMI costs across lenders: The same property and deposit can result in very different LMI quotes depending on the lender. We show you the options side by side.

- Check your eligibility for government schemes: The expanded First Home Guarantee, Family Home Guarantee, and Regional First Home Buyer Guarantee can all eliminate LMI for eligible buyers.

- Explore professional LMI waivers: If you or your partner work in an eligible profession, we'll match you with lenders that offer waivers.

- Model the buy-now vs save-longer scenario: We run the numbers to show you whether paying LMI and buying sooner is financially better than waiting to save a full 20% deposit.

- Handle the application process: From document collection to lender submission to LMI approval — we manage the entire process so you don't have to.

Ready to find out what LMI would cost you — or how to avoid it altogether? Book a free consultation with Brokio today. We'll review your deposit, income, and property goals, then build a clear plan to get you into your home with the lowest possible costs.

Disclaimer: LMI costs are estimates based on publicly available calculator data as of March 2026 and may vary between lenders. This guide provides general information only and does not constitute financial advice. Contact Brokio for personalised guidance tailored to your circumstances.