How guarantor home loans work in Australia. Learn how your parents can help you buy a house with a smaller deposit. Expert guide from Brokio, Williams Landing.

A guarantor home loan is a type of mortgage where a family member (usually a parent) offers their own property as additional security for your loan. This allows you to borrow more than you could on your own — often up to 100% of the purchase price plus costs — without paying Lenders Mortgage Insurance (LMI).

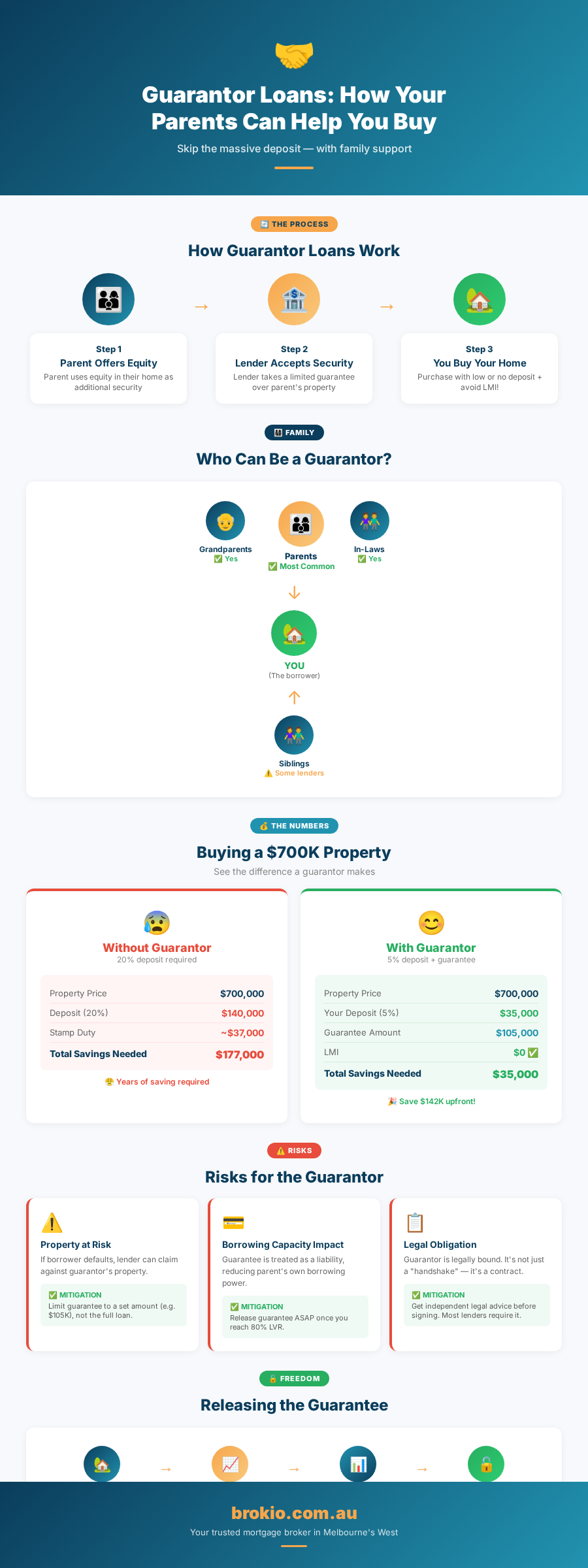

Think of it this way: instead of needing a full 20% deposit (which on a $700,000 property in Williams Landing would be $140,000), your parents' property equity acts as a "top-up" guarantee. You might only need 5% genuine savings ($35,000), with the guarantee covering the gap.

Australian property prices have outpaced wage growth for decades. In Melbourne's western suburbs, median house prices in areas like Point Cook ($700K+) and Williams Landing ($680K+) make it incredibly difficult for young buyers to save a 20% deposit while paying rent. By the time you've saved enough, prices have often moved further out of reach.

Guarantor loans bridge this gap. They allow younger Australians to enter the property market sooner, building equity through homeownership rather than paying someone else's mortgage through rent.

Guarantor loans are one of the most powerful tools available to first home buyers in Australia, and at Brokio, we help families in Williams Landing and Point Cook structure them properly every week.

Not all guarantor loans are the same. There are two main types, and understanding the difference is important for both you and your guarantor.

This is the most popular type of guarantor loan. Your parent (or family member) offers a portion of their property's equity as additional security for your loan. They don't give you money, and they don't go on your loan. Their property simply acts as extra collateral.

How it works:

With an income guarantee, your parent's income is used to supplement yours for serviceability purposes. This can help if you earn enough to make repayments but don't quite meet the lender's minimum income requirements on paper.

When this is useful:

Income guarantees are riskier for the guarantor because they're essentially vouching that if you can't make repayments, they will. For this reason, most mortgage brokers (including us at Brokio) recommend security guarantees whenever possible — they're cleaner, simpler, and easier to release later.

Most lenders structure a guarantor loan as two separate loan splits. This is important because it means the guarantee portion can be released independently once you've built enough equity, without needing to refinance the entire loan. At Brokio, we always ensure the loan is structured this way from the start — it saves you time and money down the track.

Lenders have specific rules about who can act as a guarantor. Here's what you need to know.

Most lenders accept the following family members as guarantors:

Who typically can't be a guarantor:

Your guarantor will need to meet certain criteria:

The guarantee amount is usually the difference between your deposit and 20% of the purchase price, plus any costs being financed (stamp duty, legal fees, etc.). For most first home buyers in Melbourne's west, this works out to roughly $80,000–$140,000 in guarantee — which sounds like a lot, but remember: this is just equity sitting in your parents' property. They don't hand over any cash.

Your parents' property doesn't need to be fully paid off either. As long as there's sufficient equity above their existing mortgage, they can still act as guarantor. For example, if your parents' home in Point Cook is worth $750,000 and they owe $300,000, they have $450,000 in equity — more than enough to provide a $120,000 guarantee.

Let's walk through a realistic example that many of our Brokio clients in Williams Landing can relate to.

If Sarah tried to buy without a guarantor:

By using a guarantor, Sarah:

This is a scenario we see regularly at Brokio. The numbers change, but the outcome is the same — guarantor loans help buyers get into the market sooner, without wasting money on LMI.

Let's be honest about the risks. Being a guarantor is a generous act, and it does carry some exposure. Here's what your parents (or family member) need to understand.

If you can't make your mortgage repayments and the lender needs to recover their money, the guarantor's property could be at risk. In the worst-case scenario, the lender could force the sale of the guarantor's property to recover the guaranteed amount.

Mitigation:

While the guarantee is active, lenders treat it as a contingent liability for your guarantor. This means if your parents want to refinance their own loan, buy another property, or access equity, the guarantee may reduce their borrowing capacity.

Mitigation:

Money and family can be a tricky combination. If financial pressures arise, the guarantee can create tension between family members.

Mitigation:

Most lenders require the guarantor to obtain independent legal advice before the guarantee is finalised. This is actually a great safeguard — it ensures your parents fully understand their obligations and rights. The cost is typically $200–$500 and is money well spent for peace of mind.

The good news is that a guarantor arrangement is temporary. Here's how and when you can release it.

You can apply to release the guarantee once your loan-to-value ratio (LVR) drops to 80% or below — meaning you owe 80% or less of your property's current value. This happens through a combination of:

In Melbourne's western suburbs, where property values have been growing steadily, most of our clients at Brokio release their guarantor within 2-4 years. Some manage it even sooner if they make extra repayments or if property values grow strongly.

If you don't have a family member who can act as guarantor, you still have options:

At Brokio, guarantor loans are one of our specialities. Based in Williams Landing and serving Point Cook, Tarneit, and all of Melbourne's west, we:

Ready to explore guarantor home loans? Book a free consultation with Brokio. Bring your parents along — we'll explain everything clearly so everyone feels comfortable. Call us or visit our office at 601/87 Overton Road, Williams Landing VIC 3027.

Ready to explore tailored loan options? Contact Brokio today and let us guide you through your mortgage, car loan, personal loan, or investment property loan journey with confidence.