Complete guide to business loans for Melbourne small business owners in 2026. Compare loan types, interest rates, eligibility and application tips. Expert advice from Brokio.

If you run a small business in Melbourne — whether you're a tradie in Point Cook, a café owner in Werribee, or a professional services firm in Williams Landing — there's a good chance you'll need external finance at some point. And in 2026, the lending landscape looks quite different from a few years ago.

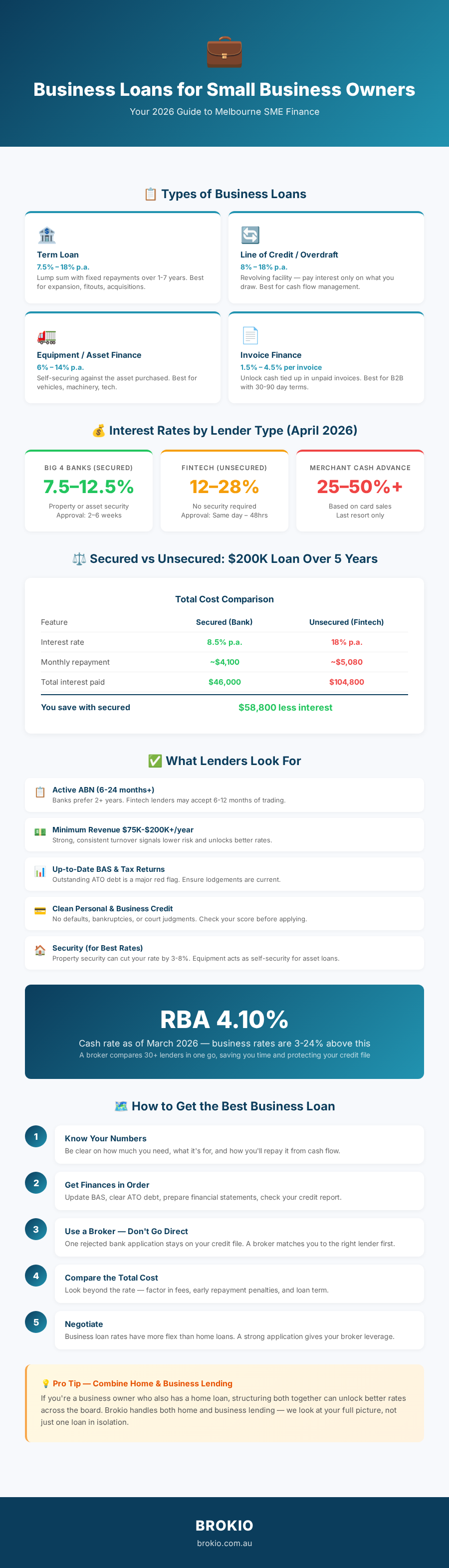

The RBA cash rate sits at 4.10% as of March 2026, following a 0.25% increase. This has pushed business lending rates higher across the board, but it's also made lenders more competitive as they fight for quality borrowers. The result? More options than ever — but bigger rate spreads between the best and worst deals.

Australia has over 2.5 million small businesses, and access to finance remains one of the biggest challenges for SME owners. The good news is that lending has evolved significantly. You're no longer limited to walking into your local CBA branch and hoping for the best. Today's market includes:

Here's what many business owners get wrong: they focus on getting any loan approved rather than getting the right loan. A business overdraft when you need a term loan, or an unsecured fintech loan when you could qualify for a much cheaper secured facility — these mistakes can cost tens of thousands in unnecessary interest.

That's where a broker comes in. At Brokio, we don't just find you a business loan — we match the right product to your specific situation, saving you money and headaches. And unlike going direct to a bank, we compare options across 30+ lenders in one go.

There's no single "business loan" — there are multiple products designed for different needs. Here's a breakdown of the main types available to Melbourne small businesses in 2026.

The most straightforward option. You borrow a lump sum and repay it over a fixed period (typically 1-7 years) with regular repayments.

A revolving credit facility attached to your business account. You only pay interest on the amount you've drawn, not the full limit.

Finance specifically for purchasing business equipment — vehicles, machinery, technology, medical equipment, tools. The asset itself acts as security.

Unlock cash tied up in unpaid invoices. The lender advances 80-90% of the invoice value, then collects from your customer.

An advance based on your future card sales. Repayments are a percentage of daily card transactions.

The Australian Government's SME Guarantee Scheme allows lenders to offer unsecured loans to small businesses with a partial government guarantee. This means businesses without property security can still access term loans up to $5 million at better rates than purely unsecured products.

Choosing between these products is one of the most important financial decisions you'll make for your business. The wrong structure doesn't just cost more — it can strain cash flow at the worst possible time.

Interest rates on business loans vary dramatically depending on the lender type, security offered, your time in business, and your financial profile. Here's the current rate landscape as of April 2026.

| Lender Type | Typical Rate (p.a.) | Security | Approval Speed |

|---|---|---|---|

| Big 4 Banks (secured) | 7.5% – 12.5% | Property/assets | 2–6 weeks |

| Big 4 Banks (unsecured) | 11% – 18% | None/limited | 1–2 weeks |

| Equipment Finance | 6% – 14% | Asset (self-securing) | 1–5 days |

| Fintech (unsecured) | 12% – 28% | None | Same day – 48hrs |

| Merchant Cash Advance | 25% – 50%+ | None | Same day |

Two businesses applying for the same loan amount from the same lender can get rates 4-6 percentage points apart. The key factors are:

With the RBA at 4.10% and market expectations of potential rate changes ahead, the fixed-vs-variable question is top of mind for business owners:

Pro tip: Don't just look at the headline rate. Factor in establishment fees ($0-$800), monthly account fees ($0-$30/month), and early repayment penalties. The total cost of the loan is what matters, not just the interest rate.

Getting approved for a business loan in 2026 requires more than just a good idea. Here's what lenders actually assess — and the minimum requirements you'll need to meet.

The level of documentation varies by lender type. Banks require the most; fintechs the least.

The most common reasons small business loan applications fail in 2026:

The broker advantage: A good broker knows which lenders suit your specific profile. At Brokio, we pre-assess your application before submitting, so we only approach lenders where you have a genuine chance of approval. This protects your credit file from unnecessary enquiries and saves weeks of back-and-forth.

This is one of the biggest decisions you'll face when borrowing for your business. Both options have clear advantages and trade-offs.

You offer an asset (usually property, but sometimes equipment or other business assets) as security for the loan. If you default, the lender can sell the asset to recover their money.

No asset is required as security. The lender assesses your business's cash flow, revenue, and creditworthiness.

Let's compare a $200,000 business loan over 5 years:

| Feature | Secured (Bank) | Unsecured (Fintech) |

|---|---|---|

| Interest rate | 8.5% p.a. | 18% p.a. |

| Monthly repayment | ~$4,100 | ~$5,080 |

| Total interest paid | $46,000 | $104,800 |

| Difference | Secured saves you ~$58,800 in interest | |

That's nearly $60,000 in savings — a significant sum for any small business. Of course, if you don't have property to offer or need funds urgently, unsecured can still be the right choice. The key is understanding the true cost before you commit.

Getting the best business loan isn't just about comparing rates — it's about presenting your business in the best possible light and approaching the right lender. Here's a step-by-step guide.

Before approaching any lender, be clear on:

The #1 reason applications stall is incomplete or messy financials. Before applying:

This is where most business owners waste time. Going direct to one bank means you only see one option. And if you get rejected, that enquiry stays on your credit file.

A broker compares options across dozens of lenders — banks, non-banks, equipment specialists, and government-backed programs — and matches you to the best fit based on your specific circumstances.

Once you've identified the right lender and product:

At Brokio, business lending is a growing part of what we do for the Melbourne western suburbs community. Based in Williams Landing, we work with small business owners across Point Cook, Tarneit, Werribee, Hoppers Crossing and beyond. Here's how we help:

Ready to explore business loan options? Book a free consultation with Brokio. We'll review your financials, identify the best lender match, and guide you through the entire process. Call us or visit 601/87 Overton Road, Williams Landing VIC 3027.

Ready to explore tailored loan options? Contact Brokio today and let us guide you through your mortgage, car loan, personal loan, or investment property loan journey with confidence.