Everything Australian small business owners need to know about business loans. Compare types, rates & eligibility. Expert broker help from Brokio — free consultation.

A business loan is a form of finance provided to businesses — from sole traders and startups to established SMEs — to fund operations, growth, equipment, cash flow, or expansion. Unlike personal loans, business loans are structured around the financial health and revenue of the business rather than just the individual borrower.

Australia has over 2.5 million small businesses, and access to the right finance is one of the single biggest factors separating businesses that grow from those that stagnate. Whether you're looking to:

…there is a business loan product in Australia designed specifically for your need. The challenge most business owners face is knowing which loan is right for them, which lender offers the best terms, and how to structure the application to maximise approval chances.

That's exactly where a specialist broker like Brokio adds enormous value — cutting through the complexity and putting the right deal in front of you without the guesswork.

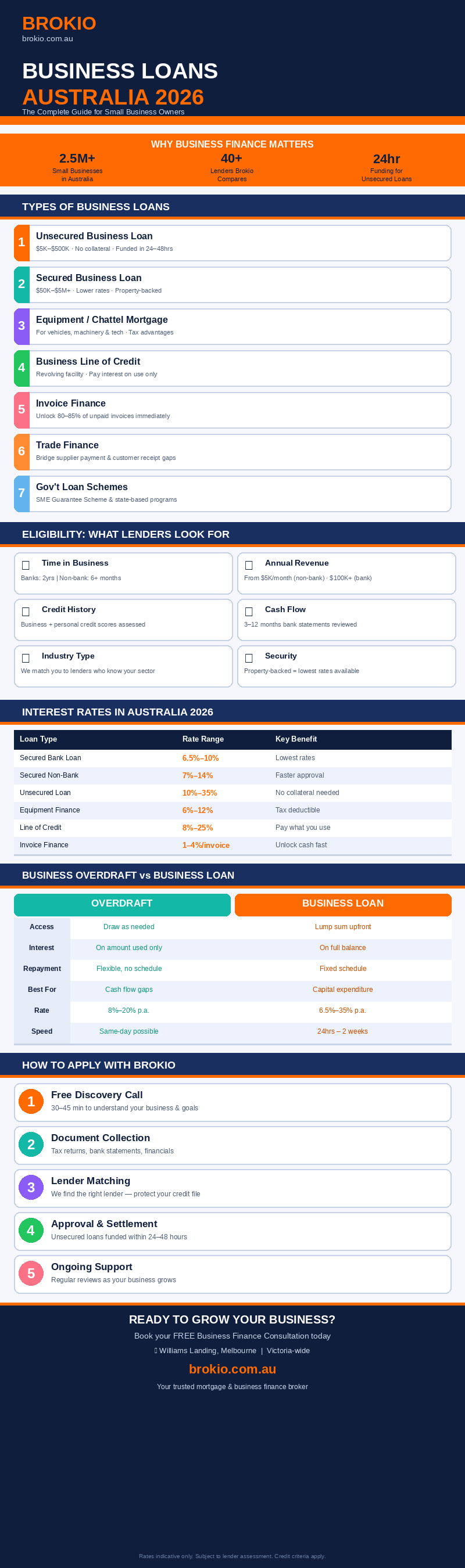

Australia's business lending market is broad, and understanding each product is critical to making the right choice. Here's a breakdown of the most common types of business loans available to Australian SMEs in 2026:

Unsecured business loans require no collateral — no property, no assets, no personal guarantee against a specific asset. Approval is based on your business's cash flow, revenue history, and credit profile. These are ideal for established businesses with strong turnover needing fast access to capital (often funded within 24–48 hours).

Secured business loans are backed by an asset — typically commercial or residential property, equipment, or vehicles. Because the lender holds security, interest rates are significantly lower and loan amounts can be much larger.

Designed specifically for purchasing business equipment, vehicles, or machinery. The asset itself acts as security, making approval straightforward. A chattel mortgage is one of the most popular business loan structures in Australia because of its significant tax advantages — GST input credits, depreciation, and interest deductibility.

A flexible revolving credit facility that lets you draw down funds as needed, repay, and redraw again — similar to how a credit card works but at much higher limits and lower rates. You only pay interest on what you use.

If your business issues invoices with 30–90 day payment terms, invoice finance lets you unlock the cash tied up in unpaid invoices immediately — typically up to 80–85% of the invoice value — rather than waiting for clients to pay.

Trade finance helps importers and exporters fund the purchase of goods. It bridges the gap between paying your supplier and receiving payment from your customer — critical for product-based businesses operating across borders.

The Australian and state governments offer a range of loan guarantee schemes and grants for eligible small businesses. The SME Guarantee Scheme and various state-based programs can provide access to finance that might not otherwise be available through traditional lending. A Brokio broker can help you identify which schemes your business may qualify for.

One of the most common questions business owners ask is: "Will I be approved for a business loan?" While every lender has different criteria, there are core factors that almost universally influence business loan eligibility in Australia.

Most traditional lenders (banks) require a minimum of 2 years of trading history. However, specialist non-bank lenders can approve businesses with as little as 6 months of trading history, making them an excellent option for newer businesses that can demonstrate strong revenue.

Lenders want to see that your business generates enough revenue to service the loan comfortably. As a general benchmark:

Both your business credit score and your personal credit score (as the director/owner) will be assessed. A strong credit history with no defaults or judgements significantly improves your approval odds and the interest rate offered.

Lenders will review 3–12 months of business bank statements to assess cash flow patterns, regular deposits, and ability to meet repayments. Consistent, growing revenue is highly favourable.

Some industries are considered higher risk by lenders (hospitality, retail, construction). Working with a broker like Brokio means we can match your business to lenders who specialise in your industry and are more likely to approve your application.

For secured loans, lenders will assess the value of the asset being offered as security. Property-backed loans generally attract the best rates and highest approval chances.

Some lenders — particularly for larger loans — will want to understand the purpose of the funds and may request a business plan or financial projections. Having these documents prepared in advance can significantly accelerate approval.

Pro tip from Brokio: Before applying with any lender, speak with a broker first. Applying directly with multiple lenders leaves multiple hard credit enquiries on your file — which can actually reduce your credit score and hurt future applications. A broker can match you to the right lender upfront, with a single application.

Business loan interest rates in Australia vary significantly depending on the lender type, loan structure, loan purpose, and your business's risk profile. Here's a general guide to what you can expect in 2026:

| Loan Type | Rate Range (p.a.) | Notes |

|---|---|---|

| Secured Business Loan (Bank) | 6.5% – 10% | Best rates for low-risk, property-backed loans |

| Secured Business Loan (Non-Bank) | 7% – 14% | Faster approval, more flexible criteria |

| Unsecured Business Loan | 10% – 35% | Higher risk to lender = higher rate; fast access |

| Equipment / Chattel Mortgage | 6% – 12% | Asset acts as security; excellent tax treatment |

| Invoice Finance | 1% – 4% per invoice | Fee per invoice, not annual rate |

| Business Line of Credit | 8% – 25% | Interest charged on drawn balance only |

Rates are indicative and subject to change. Your actual rate will depend on your business profile, loan amount, and lender assessment.

Fixed rate business loans lock in your repayment for the term — giving certainty and making cash flow planning straightforward. Variable rate loans fluctuate with the RBA cash rate and lender margin, and often come with more flexible features like early repayment without penalty.

In the current rate environment, many business owners are opting for fixed rates for certainty, especially for equipment finance and secured term loans. Brokio can model both scenarios for you and show you the true cost of each option over the full loan term.

Always compare the comparison rate, not just the headline interest rate. The comparison rate incorporates most fees and charges into a single figure, giving you a much more accurate picture of the true cost of a business loan.

Two of the most commonly confused business finance products are the business overdraft and the business loan. While both provide access to funds, they work very differently — and choosing the wrong one can cost your business thousands.

A business overdraft is a credit facility attached to your business transaction account. It allows you to spend beyond your account balance up to an approved limit. You only pay interest on the amount you actually use, and there are typically no fixed repayment schedules — you repay as cash comes into the account.

A business loan is a lump sum of money borrowed for a specific purpose, repaid over a fixed term with scheduled repayments (weekly, fortnightly, or monthly). Terms range from a few months to 30 years depending on the loan type.

| Feature | Business Overdraft | Business Loan |

|---|---|---|

| Access to funds | Revolving, draw as needed | Lump sum, upfront |

| Interest charged on | Amount used only | Full loan balance |

| Repayment structure | Flexible (no fixed schedule) | Fixed scheduled repayments |

| Best for | Short-term cash flow gaps, seasonal needs | Specific purposes, large capital expenditure |

| Typical rates | 8% – 20% p.a. | 6.5% – 35% p.a. (varies by type) |

| Approval speed | Often same day for existing customers | 24 hours – 2 weeks |

| Security required | Usually unsecured (for small limits) | Secured or unsecured options available |

In many cases, savvy business owners use both products simultaneously — a business loan for capital expenditure and an overdraft for day-to-day cash flow management. A Brokio broker will help you determine the optimal structure for your specific business situation.

Applying for a business loan through Brokio is a straightforward, streamlined process — and unlike going directly to a single bank, we compare options across 40+ lenders including major banks, non-bank lenders, and specialist business finance providers to find the deal that genuinely suits your business.

Book a no-obligation call or in-person meeting with your Brokio broker. We'll take the time to understand your business, your goals, the purpose of the loan, and your financial situation. This takes around 30–45 minutes and gives us everything we need to start identifying the right options for you.

We'll let you know exactly which documents are needed for your specific application. Typically this includes:

We make this process as painless as possible — many clients are surprised by how quickly we can move once documents are in hand.

We assess your profile against our lender panel and identify the lenders most likely to approve your application at the best available rate. We prepare and submit your application — protecting your credit file from multiple hard enquiries.

Once approved, we'll walk you through the loan offer, explain the terms clearly, and manage the settlement process. For unsecured business loans, funds can be in your account within 24–48 hours. For secured or larger loans, the timeline is typically 1–3 weeks.

Our relationship doesn't end at settlement. As your business grows, your finance needs will evolve. Brokio's clients benefit from ongoing reviews to ensure your finance structure continues to work for you — whether that means refinancing to a better rate, increasing a facility, or adding new products.

Whether you need a business loan, a business overdraft, equipment finance, or advice on the best structure for your situation — Brokio is here to help. We're based in Williams Landing and proudly serve businesses across Melbourne's west and throughout Victoria.

Book your free business finance consultation today and let's find the right finance for your business.

Ready to explore tailored loan options? Contact Brokio today and let us guide you through your mortgage, car loan, personal loan, or investment property loan journey with confidence.